$FILA.MI: A Real Pencil-Butt Investment

- Strong portfolio of over 20 brands, including Dixon Ticonderoga

- Well positioned for tariff offsetting, with 22 factories spanning six continents

- 26% stake in DOMS worth €396M, €91M of which is unrestricted

- Art supplies brands less vulnerable to obsolescence than traditional stationery

Thesis

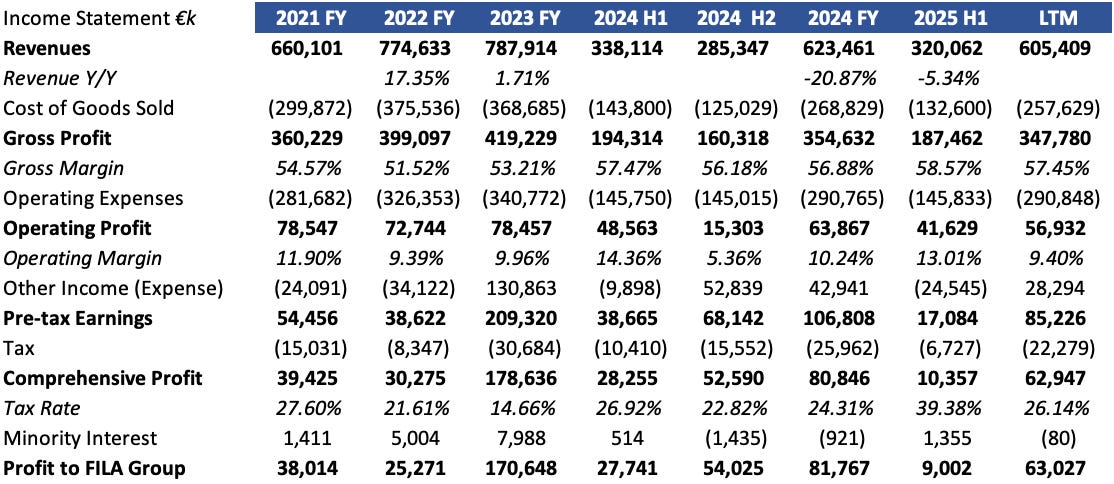

Founded in 1920 and best known for its Dixon Ticonderoga brand, FILA Group is an Italian art, school, and office supplies company with over 20 brands and customers all around the world. I believe at its current market valuation of €408M, 6.64x its LTM net income, $FILA.MI presents an attractive risk-to-reward profile, even if sales continue to decline. The company’s diversified manufacturing and the seasonal nature of its business provide it plenty of room to adapt to tariff uncertainties. The company also owns a 26.01% stake in former subsidiary DOMS worth €396M, which it has gradually sold to return cash to shareholders.

Business Overview

FILA Group is an Italian holding company with a large portfolio of stationery and art supply brands, with a focus on school supplies. The company’s largest market is in North America, making up 49% of total sales in 2024. American consumers may best know the company for its Dixon Ticonderoga brand of pencils. The company has continued to operate for over 100 years, expanding through acquisitions. It now manages a portfolio of 22 brands and owns factories across nearly every continent.

Current Position

The company has recently announced its results for the first half of 2025, continuing the single-digit revenue decline seen in the first quarter. This decline is due in part to recent cuts to education spending in both the US and UK, as well as an overall decline in consumer spending and unfavorable currency conversions. Management currently believes that the rest of 2025 will look much like the second half of the previous year, hoping for increased spending from parents to offset school budget cuts.

While demand for school and office stationery is likely to decline as digital solutions gain further adoption, this may not be a death sentence for the company. The group’s brand portfolio includes a wide selection of art supplies, which are not as easily replaced by digital alternatives.

Tariffs

FILA Group’s global manufacturing presence provides it with plenty of opportunities to reduce US import tariffs, such as shifting production to its facilities in Mexico and Canada, which currently benefit from USMCA exemptions. Due to the seasonal demand for school supplies, most of the year’s inventory was in-house by the end of April, before liberation day tariffs took effect. With replenishment beginning in August, the company has had plenty of time to adjust its operations during the off-season.

DOMS Stake

A focal point for many $FILA.MI investment theses is the company’s 26.01% stake in its former subsidiary DOMS. I had previously dismissed the possibility of this stake being sold, as management has repeatedly stated that it did not have plans to reduce its ownership below the 20% required to maintain a beneficial partnership with the former subsidiary. Recent developments and communication from management have led me to believe that this position may be sold off sooner than I previously expected. Even with the partnership’s restrictions, FILA Group still holds €91.5M of unrestricted shares.

The existing partnership provides FILA Group the exclusive right to sell DOMS products in its territories, as well as the option to outsource production to the company’s factories in India. In the most recent call, management revealed that recent tariff changes have halted plans to shift production to India, greatly reducing the utility of the partnership.

In the event of further sales, shareholders are likely to benefit from special cash dividends, as were distributed following the company’s IPO in 2023 and an additional sale in 2024.

Value Realization

FILA Group’s CEO, Massimo Candela, is the grandson of the company’s founder and currently holds 53.42% of voting rights. While at first this may be concerning for value realization, past actions such as DOMS’ spinoff, special dividends, and share repurchases indicate that the company’s management is in favor of returning cash to shareholders. The company has paid out €41.4M in dividends and share repurchases in the first half of 2025, roughly 10.15% of their market cap, and €36.5M in 2024.

Valuation

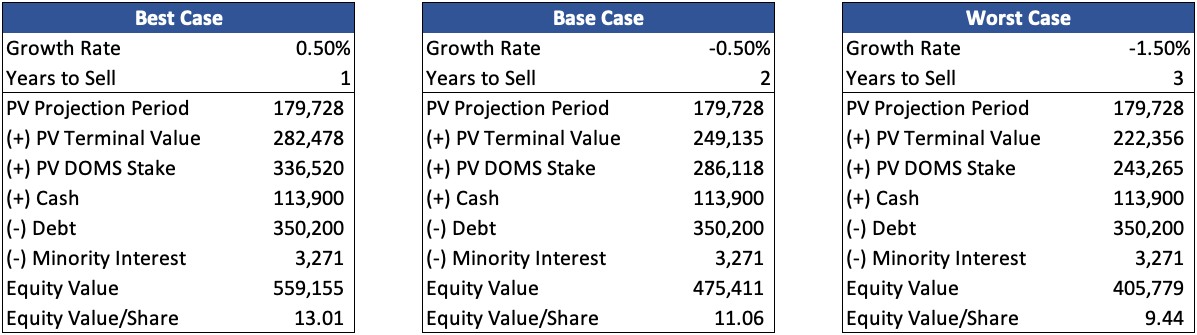

I value $FILA at €10.95/share, with a worst case of €9.49 and a best case of €12.68.

In this valuation, I project NOPAT as a proxy for free cash flow to firm, based on management expectations for sales in the second half to resemble 2024, as well as past margins. My estimate of €41M free cash flow to firm is below the latest management guidance of €40-50M free cash flow to equity. This is likely due to one-time inflows from factory closures, which I am not taking into consideration for the sake of future projections.

I project 5% lower sales for the next four years to account for the impact of tariffs and reduced educational spending. For the terminal value, I assume that the company’s sales will continue to decline at a constant rate of 0.5% per year, declining 1.5% on the low end and growing by 0.5% on the high end.

I adjusted FILA’s cost of equity to 12.72%, taking into consideration the company’s credit spread above euro-denominated bonds, as I find the stock’s beta of 0.7 does not properly reflect its level of risk. Based on outstanding loans, the company’s after-tax cost of debt is 3.93%, making for a WACC of 8.66%.

$DOMS is a recent listing on India’s national stock exchange and is trading at a very speculative valuation of 75x P/E. For this reason, I will be heavily discounting the value of FILA Group’s stake with a cost of equity of 17.62% to reflect market risk as well as uncertainty regarding if/when the company decides to sell this position. I project that the company will offload this position over the next one to three years, depending on the strategic value of the partnership.

These three scenarios leave us with a per-share value ranging from €9.44 to €13.01, equivalent to a LTM P/E ratio of 6.61x to 9.10x, compared to the current market multiple of 6.64x.

This valuation likely leans on the conservative side, at least in its assessment of how much of $DOMS’ current market value will be realized to shareholders.

Disclaimer: I am not a licensed financial advisor. Nothing on this Blog, social media, or any other platform where I post content should be considered financial advice. Any views expressed here are my own, shared for informational purposes only. Readers should conduct their own research or consult with a licensed professional before making investment decisions.